https://news.google.com/__i/rss/rd/articles/CBMiR2h0dHBzOi8vd3d3Lm55dGltZXMuY29tL2xpdmUvMjAyMS8wMS8wOC9idXNpbmVzcy91cy1lY29ub215LWNvcm9uYXZpcnVz0gFQaHR0cHM6Ly93d3cubnl0aW1lcy5jb20vbGl2ZS8yMDIxLzAxLzA4L2J1c2luZXNzL3VzLWVjb25vbXktY29yb25hdmlydXMuYW1wLmh0bWw?oc=5

The Internal Revenue Service misdirected stimulus payments for an estimated 13 million accounts, but the agency on Friday said it is trying to redirect to the money to the proper place. If you’re anticipating a stimulus payment that hasn’t yet landed, continue to monitor your bank accounts — and your snail mail.

The I.R.S. was taking “immediate steps” to get stimulus payments to the correct accounts, the agency said in a statement on Friday. “Many additional taxpayers will receive payments following this effort,” the I.R.S. added.

Here’s what happened: Millions of payments were sent to temporary accounts, which are often set up by companies like TurboTax, H&R Block and Jackson Hewitt when they prepare returns. They use the accounts when customers opt to have their preparation fees deducted from their refund, for example, allowing the tax firm to take its share and then pass on the rest.

The accounts may then be closed or become inactive — but may remain linked to the taxpayer’s I.R.S. records.

Tax prep companies have said they’re working with the I.R.S. to resolve the issue. TurboTax said affected customers can expect to receive direct deposits starting on Friday.

You can check the status of your stimulus payment through the I.R.S.’s Get My Payment tool. If it says your payment was sent to an account you do not recognize, it’s not necessarily an indication of fraud, the I.R.S. said. It might just mean you were linked to a temporary account, and you should continue to watch your bank account for a deposit.

More than 100 million stimulus payments have already been deposited directly into recipients’ accounts, the I.R.S. said. About 8 million payments will arrive in the mail on prepaid debit cards.

By law, the I.R.S. said, it must issue the stimulus payments by Jan. 15. After that, those who are entitled to a payment but haven’t received one must instead claim a credit on their 2020 returns. Filers can fill the so-called Recovery Rebate Credit on line 30 of the 2020 Form 1040 or 1040-SR.

Ford Motor said on Friday that it will idle a plant in Louisville, Ky., for one week beginning Monday because of a shortage of semiconductors that is causing disruptions in auto factories around the world.

Ford’s Louisville assembly plant operates two shifts a day, employs about 4,000 workers, and makes the Ford Escape and Lincoln Corsair sport-utility vehicles. The automaker said it would cancel a week of downtime scheduled for later in the year at the plant to leave its output unchanged for the year

A second Ford plant in Louisville has not been affected by the semiconductor shortage. That plant makes the Lincoln Navigator and Ford Explorer S.U.V.s, and the company’s F-series Super Duty pickup trucks.

Volkswagen last month warned that the semiconductor shortage would likely cause production delays at its plants in China and elsewhere. Honda and Nissan have also been affected by the shortage, according to Nikkei, the Japanese news organization.

General Motors said on Friday that it has not been affected by the shortage but is monitoring the matter closely.

Semiconductors play an increasingly important role in cars, controlling engines, brakes, transmissions, driver displays and other systems. Earlier this year, when auto sales fell because of the coronavirus pandemic, semiconductor manufacturers shifted their production to chips used for consumer electronics, Volkswagen said last month.

Auto sales have since rebounded, leading to shortages of automotive-grade semiconductors.

General Motors wants to shake up its image.

The automaker said on Friday that it would start a marketing campaign next week to highlight a new corporate logo and the battery technology it had developed for use in at least 30 electric vehicles it intended to introduce over the next five years.

The 113-year old company wants to reposition itself as a forward-looking producer of high-tech electric vehicles and to shed its reputation for being plodding and unexciting.

Company officials believe its image has hampered their efforts to compete with Tesla, the maker of luxury electric cars. Tesla and its chief executive, Elon Musk, are widely admired in the business and automotive world. The company’s reputation for innovation has helped build a following of customers, fans and investors. The stock market values Tesla at more the $800 billion, more than many large automakers combined. G.M. makes far more vehicles and is substantially more profitable but has a market value of around $60 billion.

G.M. will use the tagline, “Everyone in,” and some of the company’s ads will feature the author Malcolm Gladwell. G.M. is hoping the campaign will help “spark a mass E.V. movement,” said Deborah Wahl, the company’s global chief marketing officer.

G.M. has used its current square logo, which contains the letters “GM” against a blue background, for nearly 50 years. The new logo uses lowercase blue letters against a white square outlined by a blue border with rounded corners, designed to resemble an electrical outlet or plug.

“Our traditional logo is more severe,” Ms. Wahl said. “We felt a need to show the world a different aspect of what we are doing.”

G.M. plans to spend $27 billion over the next five years on new electric vehicles using a modular battery design that it is counting on to lower costs and make its cars and trucks more affordable and appealing. “We really believe this is an inflection point for E.V.s,” she said.

By: Ella Koeze·Data delayed at least 15 minutes·Source: FactSet

Financial markets continued to rally on Friday, fueled by bets that a Democrat-led government in Washington would robust fiscal stimulus and despite fresh evidence that the United States economy is backsliding as the pandemic surges.

The S&P 500 rose 0.6 percent, climbing further into record territory and bringing its gains for the week to 1.8 percent. The Stoxx Europe 600 was 0.7 percent higher, and the FTSE 100 in Britain rose slightly. In Asia, the Nikkei 225 in Japan closed with a gain of 2.4 percent, climbing to a level it last hit in 1990.

Though Washington continues to focus on the pro-Trump mob that overran the Capitol building on Wednesday, the investing world is instead focused on the wave of spending that could come as Democrats assume leadership of the White House and both houses of Congress

That enthusiasm also helped investors look past the Labor Department’s report on December payrolls, which showed that U.S. employers cut 140,000 jobs last month, the first drop since last spring. The weak report bolsters the argument that more economic stimulus is needed.

Stocks dipped Friday afternoon, but they recovered after President-elect Joseph R. Biden Jr. said he was targeting “trillions of dollars” in spending. “We should be investing significant amounts of money right now, to grow the economy,” he said.

At the same time, few on Wall Street seem to think Democrats will prioritize tax increases, which had previously been seen as a potential risk of a Democratic sweep.

“Now you have the potential for more stimulus, even possibly an infrastructure spend,” said Kristina Hooper, chief global market strategist at the investment management firm Invesco on Thursday. “So, I think the stock market is enthused right now. And that enthusiasm is pretty strong.”

Gains continued in other financial markets too. Oil prices continued to rally, with West Texas Intermediate rising more than 3 percent to $52.52 a barrel. A surge earlier in the week, which came after Saudi Arabia said it would cut production, means oil prices rose more than 8 percent this week.

The yield on the benchmark 10-year Treasury note also continued to rise, reaching 1.11 percent on Thursday. The rise in yields most likely reflects expectations that the Treasury will be issuing large amounts of debt to finance renewed government spending.

The already sputtering economic rebound went into reverse in December, as employers laid off workers amid rising coronavirus cases and waning government aid.

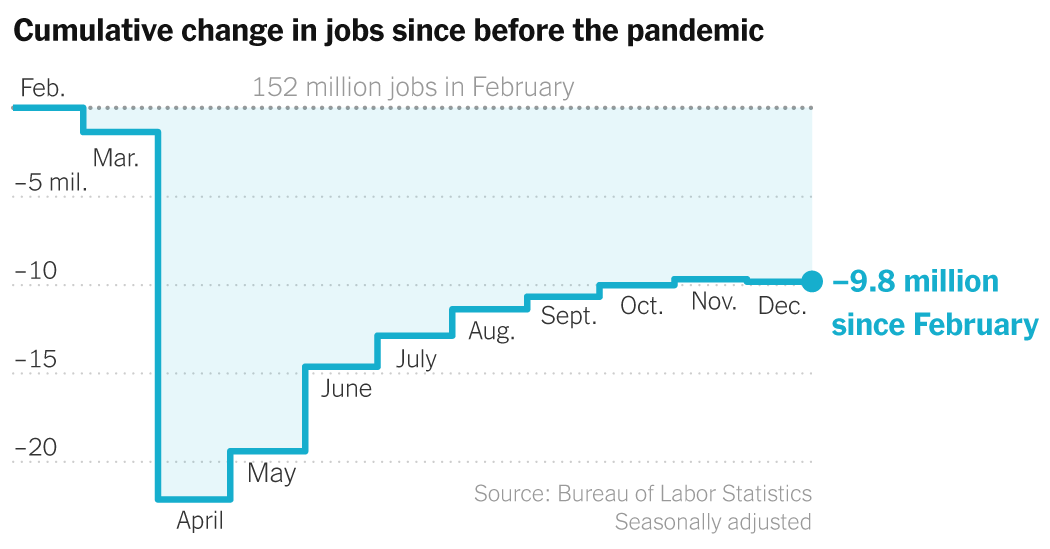

U.S. employers cut 140,000 jobs in December, the Labor Department said Friday. It was the first net decline in payrolls since last spring’s mass layoffs, and though the December loss was nowhere near that scale, it represented a discouraging reversal for the once-promising recovery. The U.S. economy still has about 10 million fewer jobs than before the pandemic began.

Job growth reversed for the first time since April

Cumulative change in all jobs since before the pandemic

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

The December losses were heavily concentrated in leisure and hospitality businesses, which have been hit especially hard by the pandemic. The industry cut nearly half a million jobs in December, while sectors less exposed to the pandemic continued to add workers.

The unemployment rate was unchanged at 6.7 percent, down sharply from its high of nearly 15 percent in April but still close to double the 3.5 percent rate in the same month a year earlier.

“We’re losing ground again,” said Diane Swonk, chief economist at the accounting firm Grant Thornton. “Most notably, this is still very much a low-wage recession, and the losses were where we first saw them when the pandemic hit.”

Unemployment rate

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

Hiring has slowed every month since June, and the economy lost more than nine million jobs in 2020 as a whole, the first calendar-year decline since 2010 and the worst on a percentage basis since the aftermath of World War II.

Congress last month passed a $900 billion relief package that will provide temporary support to households and businesses and could give a boost to the broader economy. And in the longer run, the arrival of coronavirus vaccines should allow the return of activity that has been suppressed by the pandemic.

But the vaccine and the aid came too late to prevent a sharp slowdown in growth.

“We did have a pullback in the economy,” said Michelle Meyer, head of U.S. economics at Bank of America. “If stimulus was passed earlier, maybe that could have been avoided.”

Why did job growth go into reverse? It’s simple: the resurgent pandemic.

As virus cases rose across the country in the fall, governors and mayors reimposed restrictions on businesses and consumers pulled back on activity. Job losses soon followed: Restaurants and bars cut 372,000 jobs in December. Hotels cut 24,000 more. Private schools and colleges cut more than 60,000.

The leisure and hospitality industry was hit hard in December while other sectors made small gains

Cumulative change in jobs since before the pandemic, by industry

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

“It’s more pandemic-induced job loss,” said Nick Bunker, head of North American research for the career site Indeed. “It’s a really vivid demonstration that the labor market can’t bounce back in any sustainable form until the pandemic is under control.”

Industries less exposed to the virus, on the other hand, mostly kept hiring. Manufacturers added 38,000 jobs. Construction companies added 51,000. Even retailers, hit hard in the spring but able to adapt more readily, added 120,000.

Mr. Bunker said the hiring in those areas was encouraging, suggesting that the economic damage was contained and potentially allowing for a faster rebound once the pandemic was under control.

But the concentration of job losses also means that low-wage workers, many of them Black or Hispanic, are again bearing the brunt of the crisis.

“It’s reinforcing the inequality that already happened a few months ago,” Mr. Bunker said. “It’s just hitting the people who have already been hit pretty hard.”

The girl with the golden arm will live on.

Roku, the streaming platform, said on Friday that it had agreed to buy the rights to a content library originally created for Quibi, the much-hyped short-form start-up that closed just six months after its introduction.

The deal gives Roku, which makes streaming devices but also has a popular free streaming channel, a slew of original shows and films featuring well-known Hollywood stars such as Kevin Hart, Liam Hemsworth, Anna Kendrick and Idris Elba.

Quibi’s content library has about 75 shows and documentaries, which will appear for free on the Roku Channel throughout 2021. The deal gives Roku the rights to stream the content only for seven years, after which ownership reverts back to the producers of each show.

Roku did not disclose the price of the transaction, but a person familiar with the details said it was under $100 million.

Roku generates most of its money from advertising — it gets a cut of ad dollars from the ad-supported streaming channels on its device and it also owns the Roku Channel. But free ad-based streaming services is a tough business. Roku is still not profitable on an annual basis and analysts expect it won’t be in the black till 2022.

Started by Jeffrey Katzenberg and Meg Whitman, Quibi raised more than $1.75 billion from major Hollywood studios and other investors. The service was a quixotic attempt to capitalize on the streaming boom. Its shows, chopped into installments no longer than 10 minutes, were meant to be watched on smartphones.

But the pandemic dampened the appeal for that kind of viewing as people stayed home. Its unusual format and some of its creative choices, including a show starring the Emmy-winning actress Rachel Brosnahan as a character obsessed with her own golden arm, drew some ridicule.

Rob Holmes, the head of programming at Roku, said this “isn’t the start of a big push into original production,” but the addition of original shows gives the company more options. But later on down the line, it’s possible the company could fund more productions. “We’ll see,” he said.

When the economy shut down last spring, many workers thought they would be out of a job for a few weeks, maybe a couple of months.

Nine months later, many still aren’t back on the job.

The Labor Department’s monthly jobs report on Friday showed that nearly four million Americans had been out of work for more than six months, economists’ standard threshold for long-term unemployment. That was up by 27,000 from November, and roughly quadruple the number before the pandemic began.

Those figures almost certainly understate the scope of the problem. People who aren’t looking for work, whether because they don’t believe jobs are available or because they are caring for children or other family members, aren’t counted as unemployed.

The number of people who have been unemployed long-term is still rising

Share of unemployed who have been out of work 27 weeks or longer

By Ella Koeze·Seasonally adjusted·Source: Bureau of Labor Statistics

When the data was collected in mid-December, many of the long-term jobless faced a frightening deadline: Federal programs that extended unemployment benefits beyond their standard six-month limit were set to expire at the end of the year. The aid package later passed by Congress and signed by President Trump extended the programs, but by less than three months.

Long-term joblessness was a defining feature of the last recession a decade ago, when millions eventually gave up looking for work, in some cases permanently. If that pattern repeats, it could have long-term consequences, particularly for people with disabilities, criminal records or other characteristics that make it hard to find jobs even in the best of times.

“These are the kinds of workers who are really only recruited and called upon in a very tight labor market, and it may take us a long time to get back there,” said Julia Pollak, a labor economist with the hiring site ZipRecruiter. “That is the worry, that there are these groups of people who will drop out now and who will only really find good opportunities again after a sustained and lengthy expansion.”

December’s job losses hit different demographic groups unevenly

Unemployment rates for Black, Hispanic, Asian and white workers

Unemployment rates for men and women

By Ella Koeze·Rates are seasonally adjusted except those for Asian men and women.·Source: Bureau of Labor Statistics

Unemployment rates for Hispanic workers shot up in December, even as the jobless rate moderated for Black workers and held roughly steady for whites, showing that the costs of recent job losses were being felt unevenly across demographic groups.

The Hispanic or Latino unemployment rate jumped to 9.3 percent from 8.4 percent in November, partly reversing a rapid recovery since the figure popped to 18.9 percent in April. Before the pandemic, the Hispanic jobless rate was hovering around 4.4 percent.

At the same time, the Black unemployment rate continued a gradual decline, falling to 9.9 percent in December from 10.3 percent the month before. Unemployment for Black workers didn’t jump quite as high early in the pandemic — it peaked at 16.7 percent in April and May — but it has been easing more slowly than Hispanic joblessness.

A major concern throughout the pandemic has been the economic burden falling on those with the fewest resources to weather it. Job losses have been heavy in service businesses, particularly in relatively low-wage occupations that disproportionately employ racial and ethnic minorities.

White workers have been faring better than other groups. Their unemployment rate ticked up slightly to 6 percent in December, from 5.9 percent in November, but is down from a peak of 14.1 percent last year. Still, that is about twice the 3 percent rate last February.

Asian workers are also doing comparatively well, with their unemployment rate at 5.9 percent in December, though that’s up from 2.4 percent in February.